How a bank account validation service works: validation vs verification, the four methods, real costs, the Nacha WEB debit rule and choosing a provider in 2026.

Table of contents

- A bank account validation service confirms an account number and routing code are real, open, and owned by the expected party before money moves, cutting failed payments, returns, and fraud.

- Validation checks structure and existence; verification goes further and proves ownership and status. Vendors blur the two, so always ask what each tier actually checks.

- Four methods dominate: micro-deposits, instant account verification, open banking APIs, and database or network lookups. They differ on speed, cost, ownership proof, and friction.

- Nacha's WEB Debit Account Validation Rule, effective 19 March 2021, makes a commercially reasonable validation method mandatory for first-use consumer ACH debits, and is technology-neutral on how you meet it.

- The criterion incumbents skip is data architecture. The IDMerit leak (discovered November 2025, around one billion records per Cybernews) shows why a centralised validation database is a breach honeypot.

A bank account validation service confirms that a bank account number and routing code are real, open, and owned by the expected person or business before money moves. It checks account status, ownership, and fraud risk in near real time using methods such as micro-deposits, instant account verification, or open banking, reducing failed payments, returns, and fraud.

TL;DR

A bank account validation service confirms an account is real, open, and owned by the expected party before a payment runs, using micro-deposits, instant account verification, open banking, or a database lookup. Validation checks the number and routing code; verification proves ownership and status. Nacha's WEB Debit Account Validation Rule has made a commercially reasonable method mandatory for first-use consumer ACH debits since March 2021, and is neutral on which method you pick. Costs run from cents to a couple of dollars per check, but failed-payment fees and fraud dwarf the per-check price. The criterion most buyers miss is data architecture: whether the provider stores your customers' identity data centrally, where one breach exposes it all.

What is a bank account validation service?

A bank account validation service confirms that a bank account number and routing code are real, open, and owned by the expected person or business before money moves. It checks account status, ownership, and fraud risk in near real time using methods such as micro-deposits, instant account verification, or open banking, reducing failed payments, returns, and fraud. Some providers label it AVS, or account validation services, but the job is the same: answer three questions before a transaction settles. Is this account real? Is it open and able to send or receive an ACH entry? Does it belong to the person or business in front of you?

The reach varies by provider. Many cover domestic ACH rails through routing or ABA numbers, while broader platforms validate IBAN, BIC, and national clearing codes across many countries; treat any single coverage number as a vendor claim and check the published list. What stays constant is the purpose. Account validation is a payment-accuracy and fraud control that sits at the front of disbursement, payroll, accounts payable, and onboarding flows, where a wrong digit or a closed account turns into a returned payment, a remediation ticket, or a fraud loss. The deeper you push past format checking, the more identity data enters the flow, which is the part this guide returns to.

Validation vs verification: what is the difference?

Validation and verification get used interchangeably in vendor marketing, but they answer different questions, and the gap between them is where assurance lives. Validation confirms that the structure of an account number, routing code, or IBAN is correct and compatible with the payment rail. It catches typos before a disbursement, a payroll run, or an accounts payable batch goes out, and it is cheap and instant. What it does not do is prove anyone owns the account. Verification goes further: it confirms the account is real, open, and controlled by the expected individual or business, which is the part that reduces fraud and regulatory exposure.

The practical risk is buying a validation tier and assuming it gives you verification assurance. The table below sets the two apart so you know which question each answers.

| Dimension | Validation | Verification |

|---|---|---|

| What it confirms | Format and existence of the account or routing number | Account is open and controlled by the expected party |

| Assurance level | Lower; catches errors | Higher; catches fraud |

| Ownership proof | No | Yes |

| Typical speed | Instant | Seconds to days, by method |

| Best at preventing | Typos and failed payments | Account fraud and misdirected funds |

When you scope a provider, ask exactly what each tier checks rather than trusting the label. A service that "validates" may only confirm a routing number resolves to a real bank, which is a long way short of proving the account belongs to your customer.

How does bank account verification work?

Bank account verification runs as a short pipeline, and knowing the steps tells you where assurance and risk each enter. First, you collect the account and routing number or IBAN from the customer. Second, the service runs structural or format validation to confirm the number is well-formed and the routing code resolves to a real institution. Third, it performs a status check to confirm the account is open and eligible for the rail, such as able to receive an ACH entry. Fourth, it attempts an ownership match against the named individual or business. Fifth, it returns a result, often with a fraud-risk score attached.

Speed depends on the method. Instant approaches return a result in seconds; micro-deposits take up to five business days because they wait on the customer to read two test deposits. The fourth step, the ownership match, is where personal data enters the picture: most flows transmit a name plus account details to a third-party database to confirm the link. J.P. Morgan's Account Validation API, for example, lets clients verify account status, authenticate the account owner, confirm account access, and assess fraud risk in a single call, and it returns an Account Confidence Score, an AI and machine-learning estimate of fraud likelihood. J.P. Morgan states plainly that using that score does not satisfy any KYC, AML, or sanctions requirement, a useful reminder that account validation and identity compliance are separate jobs.

What are the four main validation methods?

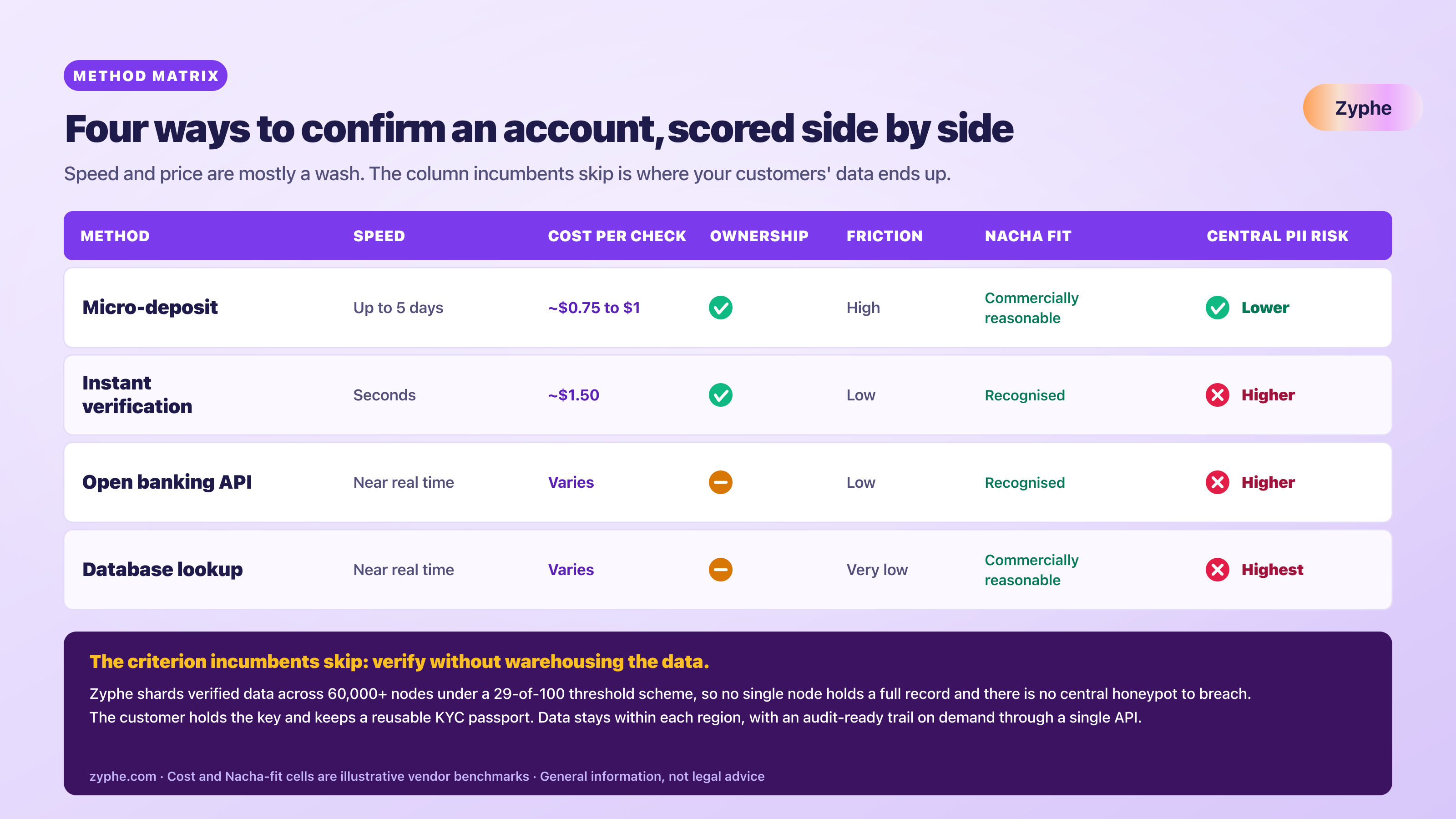

Four methods cover almost every account validation service on the market. They trade speed against assurance, cost against friction, and, the criterion most comparisons omit, retained data against breach exposure.

Micro-deposit verification

The provider sends two small ACH test deposits to the account, then asks the customer to confirm the amounts. Matching the amounts proves the customer can access the account, which is real ownership evidence. The cost is time: it takes up to five business days, and the back-and-forth drives abandonment. Cornerstone Advisors, cited by MX, found ACH-funding abandonment of 13 percent at institutions that do not require micro-deposits versus 27 percent at those that do, a more credible split than the round 20 percent often quoted. Micro-deposits suit lower-volume, lower-urgency flows where the wait is tolerable.

Instant account verification

Instant account verification, often credential-based, connects to the account in real time through a login or a tokenised connection and returns ownership and status in seconds. It removes the multi-day wait and cuts drop-off sharply; vendors commonly cite around 5 percent abandonment, though that figure traces to provider estimates rather than a primary source. The trade-off is data: a credential-based connection routes account and identity data, and sometimes login credentials, through a centralised third party.

Open banking and API verification

Open banking uses a consumer-permissioned API connection to read account data directly from the bank, with near-zero wait and no test deposits. It is used by major payment platforms for funding and verification flows. In the United States, note that the open-banking regime is unsettled: the Consumer Financial Protection Bureau's Section 1033 Personal Financial Data Rights rule, finalised in October 2024, is not currently in force. A federal court enjoined enforcement on 29 October 2025 while the Bureau reconsiders it, so treat open banking as a working method rather than a mandated data-access right today.

Database or network lookup

This method checks an account number and status against an industry database or network rather than touching the account itself. It is fast and low-friction, returns a status and often a risk signal, and underpins many "account validation services" sold by banks and fraud vendors. The catch is that it depends on a large, standing store of account and identity data, which is exactly the architecture that turns into a breach target.

| Method | Speed | Cost per check (illustrative) | Ownership proof | User friction | Nacha fit | PII retention exposure |

|---|---|---|---|---|---|---|

| Micro-deposit | Up to 5 business days | ~$0.75 to $1 (vendor benchmark) | Yes | High | Listed as commercially reasonable | Lower |

| Instant account verification | Seconds | ~$1.50 (vendor benchmark) | Yes | Low | Recognised | Higher |

| Open banking API | Near real time | Varies by aggregator | Partial to yes | Low | Recognised | Higher |

| Database or network lookup | Near real time | Varies by provider | Partial | Very low | Listed as commercially reasonable | Highest |

The cost and abandonment figures here are illustrative vendor benchmarks, not primary-sourced facts; the last column is the one incumbent comparisons leave out, and it reframes a speed-and-price decision as an architecture one.

How much does a bank account validation service cost?

Per-check pricing for a bank account validation service is modest, but the headline number hides the real cost. Vendor benchmarks from providers such as Signzy, MX, and Trustpair put micro-deposits at roughly $0.75 to $1 per transaction and instant account verification at around $1.50, with some sources placing instant methods below the all-in cost of a micro-deposit once delays are counted. Treat these as illustrative ranges, not fixed rates: they come from vendor blogs, not regulators, and real pricing depends on volume, coverage, and the assurance tier.

The costs that move the budget sit underneath the per-check line. A failed or returned ACH entry carries a return fee and a manual remediation ticket; a multi-day micro-deposit wait costs you conversions, as the Cornerstone Advisors abandonment figures show; and a missed ownership check costs you the fraud loss itself. Account validation is one input into a wider onboarding cost, so weigh it against your compliance overhead rather than the sticker price alone. Zyphe's own benchmark puts decentralised verification at a materially lower compliance cost than a conventional stack, a fraction of the cost of a conventional stack once retention and remediation overheads are counted; that is a Zyphe figure from a Zyphe model, not an independent fact, and it is offered here as a contextual benchmark rather than a neutral claim.

Is instant bank verification safe?

Instant bank verification can be fast and secure, but the question that matters is not speed; it is what happens to the data afterwards. Credential-based instant verification and database lookups both require sharing account numbers, names, and sometimes login credentials with a centralised third party. That party retains a copy. Every centralised validation database is therefore a breach honeypot: when the vendor is compromised, every account and identity it has ever validated is exposed at once. This is not an abstract risk, and the evidence is dated and specific.

On 11 November 2025, security researchers at Cybernews found an unprotected MongoDB database, with no password, tied to the identity-verification provider IDMerit. By Cybernews's count it exposed around one billion personally identifiable records across 26 countries, roughly 203 million in the United States and 124 million in Mexico, including full names, addresses, national identification numbers, dates of birth, contact details, and KYC and AML verification logs. The database was secured the next day, and there is no public evidence it was downloaded by criminals; IDMerit disputes the one-billion figure, per Biometric Update. The scale is contested, the architecture lesson is not. A second case makes the same point: a breach at the KYC provider Sumsub surfaced in a January 2026 internal audit and was disclosed in early February 2026, having gone undetected for around 18 months, after an attacker reached a third-party support platform through a malicious attachment in July 2024, exposing mostly names with a smaller subset of contact data. Two named incidents at identity vendors, one year apart, both trace back to the same flaw: a standing central store of verified identity data. The architecture, not the method, is the differentiator. You can confirm an account belongs to a person without a third party permanently retaining that personal data, a point the provider section returns to.

What does the Nacha WEB debit rule require?

Nacha's Supplementing Fraud Detection Standards for WEB Debits Rule became effective on 19 March 2021 and makes account validation an explicit part of a "commercially reasonable fraudulent transaction detection system". At minimum, an Originator must use a commercially reasonable means to determine that the account number used for a first-use WEB debit, a consumer ACH debit authorised online, is for a valid, meaning legitimate and open, account at the Receiving Depository Financial Institution to which ACH entries may be posted. Nacha granted a one-year non-enforcement grace period for entities working in good faith, so practical enforcement began in March 2022.

Nacha is technology-neutral on how you meet the standard. Its listed commercially reasonable examples include a Prenotification Entry, ACH micro-transaction verification, a commercially available validation service provided by an Originating Depository Financial Institution or a third party, and account validation services enabled by APIs; other methods may also qualify. The obligation is tightening from there. Nacha's 2026 Risk Management and Fraud Monitoring rules phase in across two stages: Phase 1 took effect on 20 March 2026 for Originating Depository Financial Institutions of all sizes and for larger non-consumer Originators, Third-Party Service Providers, and Third-Party Senders by 2023 volume; Phase 2 takes effect on 19 June 2026, practically Monday 22 June 2026 as 19 June is a federal holiday, removing the volume threshold so every non-consumer Originator, Third-Party Service Provider, and Third-Party Sender must comply. Account validation is now a baseline ACH control, not an optional upgrade. For the wider monitoring picture, see our AML transaction monitoring guide.

How does validation differ from KYC, KYB and AML?

Account validation is not identity verification, and conflating the two leaves a compliance gap. Validation proves a bank account is real and owned. Know Your Customer (KYC) proves a human is who they claim to be. Know Your Business (KYB) does the same for a legal entity and its beneficial owners. Anti-Money Laundering (AML) screening checks a customer against sanctions lists, politically exposed person lists, and adverse media. These are layers, not substitutes, and a mature onboarding stack runs all of them.

The link between them is the Customer Identification Program (CIP). Under the Financial Crimes Enforcement Network's CIP rule for banks, set out at 31 CFR 1020.220 under the Bank Secrecy Act, an institution must use risk-based procedures to form a reasonable belief that it knows a customer's true identity, collecting at minimum a name, date of birth for individuals, address, and an identification number. Account ownership verification can be one signal feeding that belief, but it is not the CIP itself; CIP is identity verification, distinct from bank account validation. The cleanest way to think about it: validation answers "is this the right account", KYC and KYB answer "is this the right person or business", and AML answers "should we be doing business with them at all". For the identity side, our KYC software and KYB software pages show how the checks fit together, and the decentralised KYC explainer covers running them without warehousing the data.

How do you choose a bank account validation service?

The provider landscape in 2026 splits into rough categories, and naming them keeps the comparison honest. Bank-direct services come from institutions such as J.P. Morgan and U.S. Bank. Open-banking and API aggregators such as Plaid, GoCardless, and MX sell consumer-permissioned connections. Fraud and accounts payable specialists such as Trustpair, Eftsure, GIACT, and nsKnox focus on payment integrity. Identity-led platforms such as Persona, LexisNexis Risk, and Signzy bundle validation into wider onboarding. Each is good at something, and each makes a different trade-off on how much of your customers' data it retains. Use the checklist below to pressure-test any of them; it is a starting point, not legal advice.

- ] Coverage: which countries, rails, and identifiers (ABA, IBAN, BIC) does it actually validate, per published docs?

- ] Speed against assurance: does the tier you are buying prove ownership, or only format and existence?

- ] Ownership proof depth: validation, verification, or a fraud score, and what does each return?

- ] Nacha fit: is the method a commercially reasonable one for first-use WEB debits and the 2026 fraud-monitoring rules?

- ] Fraud scoring: is a risk signal returned, and is it clearly separated from any KYC or AML claim?

- ] Fallback: what happens when an instant check fails and you need a second method?

- ] Pricing model: per-check, tiered, or subscription, and how do return fees and remediation land?

- ] Data architecture: does the vendor retain your customers' personal data centrally, or verify without storing it?

That last item is the one incumbents rarely raise, because it is the one where most of them are exposed. A central store of validated accounts and identities is an asset to the vendor and a liability to you the day it is breached, as IDMerit and Sumsub showed. This is where a privacy-first design changes the question. Rather than route identity data into another central database, the approach is to confirm an account belongs to a person while no single system holds the complete record. Zyphe shards verified data across a decentralised network of more than 60,000 nodes under a 29-of-100 threshold scheme, so no single node holds a full record and there is no central honeypot to breach, while authorised parties can still reconstruct a complete record and export an audit-ready trail on demand. The customer keeps a reusable KYC passport they can re-present elsewhere, verification runs through a single API in around fifteen minutes of integration, and data stays within each region. The steelman for the incumbents is fair: a well-run central store in a SOC 2 environment, encrypted at rest and minimised, passes audits every day, and many buyers will reasonably accept that model. The counter is just as simple. Encryption at rest does not stop a bribed insider or a misconfigured database left open to the internet, and retention rules force you to keep the data for years. If your build can avoid holding the honeypot at all, that is one fewer breach headline waiting to happen. If that architecture fits your onboarding, you can book a demo to map it to your flow.

The bottom line

A bank account validation service is now a baseline payments control, not a nice-to-have: Nacha has made a commercially reasonable method mandatory for first-use ACH debits, and the 2026 fraud-monitoring rules pull more firms into scope. Picking a method, micro-deposit, instant, open banking, or database lookup, is mostly a speed-against-assurance call, and the per-check price is the small number. The bigger decision is the one most comparisons avoid. Validation accuracy is table stakes; whether the provider turns your customers' identity data into a central breach target is the differentiator. Choose the method your flow needs, then ask the architecture question before you sign.

Related resources

- Why your KYC vendor is your biggest data breach risk

- Decentralised KYC: what it is and how it works

- AML transaction monitoring guide

- Proof of address verification

- Zyphe KYC software

- Zyphe KYB software

Cited sources

- Nacha, Supplementing Fraud Detection Standards for WEB Debits Rule (effective 19 March 2021)

- Nacha, Risk Management Topics: Fraud Monitoring Phase 2 (2026 effective dates)

- J.P. Morgan Payments Developer Portal, Account Validation capabilities

- Electronic Code of Federal Regulations, 31 CFR 1020.220 Customer Identification Program (FinCEN, Bank Secrecy Act)

- Cozen O'Connor, Section 1033 open banking rule enjoined and under reconsideration

- Cybernews, Global data leak exposes around one billion records (IDMerit, November 2025)

Michelangelo Frigo (Co-Founder at Zyphe) Michelangelo Frigo is a privacy and identity infrastructure expert and co-founder of Zyphe.

Michelangelo Frigo (Co-Founder at Zyphe) Michelangelo Frigo is a privacy and identity infrastructure expert and co-founder of Zyphe.