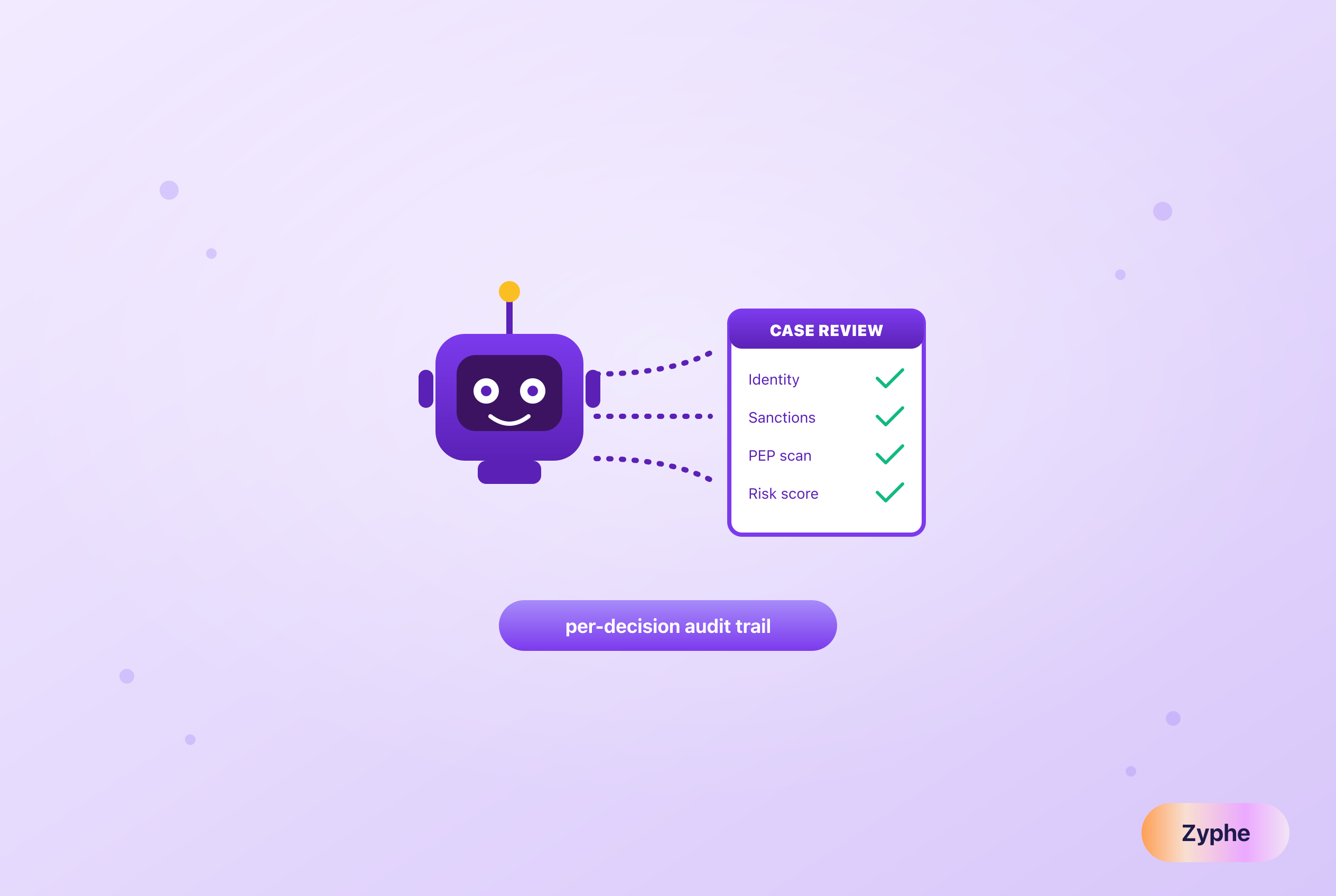

AI compliance agents run L1 triage, EDD, UBO mapping and KYB refresh with reasoning AI inside Unit21, Jira and Salesforce, with audit trails regulators accept.

Table of contents

Key highlights

- In October 2024, TD Bank pleaded guilty and paid roughly $3 billion to the US Department of Justice and FinCEN after admitting it left more than 90 percent of its transaction activity, some $18.3 trillion, unmonitored. That was a review-capacity failure, not a data failure.

- AI compliance agents are reasoning systems that log into your existing KYC, KYB, AML, and case-management tools, complete reviews end to end, and produce a per-decision audit trail.

- They are not robotic process automation. RPA replays fixed clicks; a reasoning agent reads the source records, weighs typology fit, cites its evidence, and knows when to escalate.

- Agents work today on five surfaces: L1 sanctions and PEP triage, L2 case completion, enhanced due diligence, ultimate beneficial owner chain resolution, and KYB periodic refresh.

- They are deployed inside Unit21, Jira, Salesforce, and similar systems, not as a parallel tool, so the work and the audit trail stay where examiners already look.

- Model governance is the gating question. Treat an agent as a model under SR 11-7 and the NIST AI Risk Management Framework, with version control, decision logging, and human attestation on anything filed.

AI compliance agents are reasoning systems that log into existing KYC, KYB, AML, and case-management tools, complete reviews end to end, and produce a per-decision audit trail. Unlike rule-based automation, they read the underlying source records, weigh typology fit, cite the evidence behind each decision, and escalate the cases that genuinely need human judgement.

TL;DR

AI compliance agents are reasoning systems that log into existing KYC, KYB, AML, and case-management tools, complete reviews end to end, and produce a per-decision audit trail. They are the operational answer to a problem that fines keep exposing: not a shortage of data, but a shortage of review capacity. When TD Bank left more than 90 percent of its transaction activity unmonitored, the data existed. Nobody and nothing reviewed it at the scale required.

This pillar explains what separates a reasoning agent from the robotic process automation that failed at this job, the five review surfaces agents handle today, why they belong inside your existing tools rather than beside them, and how to govern them under SR 11-7 and the NIST AI Risk Management Framework so the output survives an examination.

15 min read. Last updated 17 June 2026.

What is an AI compliance agent?

An AI compliance agent is a reasoning system that does the review work a junior analyst does, end to end, inside the tools your team already uses. It authenticates into your case-management system, opens an alert or a case, pulls the underlying transaction and source records, evaluates them against the relevant typology, writes a disposition with its reasoning, and either closes the item or escalates it. Crucially, it logs why it reached each decision, with citations back to the records it relied on.

That last property is what makes it a compliance tool rather than a productivity gadget. A compliance decision is only as good as its defensibility, so an agent that cannot show its evidence is useless to a regulated firm. The agents worth deploying in 2026 produce structured, cited output a reviewer and an examiner can follow. For the monitoring layer these agents operate on, our guide to AML transaction monitoring in 2026 sets the baseline.

Why did traditional RPA fail at L1 alert triage?

Robotic process automation promised to clear alert backlogs a decade ago, and it did not, because triage is a judgement task wearing a clerical disguise. RPA replays a fixed sequence of clicks. It cannot read a transaction it has not been scripted for, cannot weigh whether a name match is the same person, and cannot write a defensible rationale. So firms automated the easy 20 percent and left analysts drowning in the rest.

TD Bank is the cautionary scale. Between January 2018 and April 2024, the bank admitted that more than 90 percent of its transaction activity went unmonitored, roughly $18.3 trillion, and three money-laundering networks moved more than $670 million through its accounts as a result. The Department of Justice took a $1.43 billion criminal penalty plus $452.4 million in forfeiture, and FinCEN imposed a $1.3 billion civil penalty, its largest ever against a depository institution, with a four-year independent monitorship attached. Read it the right way: the failure was not missing data, it was missing review at scale. Rules and RPA could not close that gap. Reasoning can.

What does "reasoning" actually mean in compliance?

"Reasoning" is an overused word, so here is the operational definition that matters for a regulated firm. A reasoning agent does three things a rules engine cannot.

It interprets unstructured and semi-structured evidence, reading the source transaction, the customer record, and the screening hit, rather than matching a field to a threshold. It produces structured output, a typology classification, a confidence, and a written rationale, in a form your case system can store and your QA team can sample. And it cites, attaching each material claim to the specific source record it came from, so a reviewer can trace the decision rather than trust it.

Model lineage sits underneath all three: which model version produced the decision, on what prompt, over which documents. Without lineage you cannot reproduce or defend a disposition, which is why the agents that hold up in examination are built around logged, versioned reasoning rather than a black box that simply returns "clear" or "escalate."

Which review surfaces do AI compliance agents work on today?

Agents are not a single product. They are a pattern applied to specific review surfaces, and five are in production use now.

L1 sanctions and PEP triage is the first and highest-volume surface

This is the backlog factory, where more than 90 percent of alerts are false positives. An agent fetches the hit and the underlying record, scores the match, and disposes the clear-cut majority with a written rationale, escalating the genuine candidates. Our companion piece on L1 alert triage with AI goes deep on this surface.

L2 case completion is where partial cases get finished

Agents assemble the evidence, draft the case narrative, and prepare the package for a human decision, compressing hours of assembly into minutes.

Enhanced due diligence is research at scale

For higher-risk customers, an agent gathers corporate, ownership, and adverse-media evidence into a structured EDD file rather than a junior analyst spending a day in tabs.

UBO chain resolution untangles ownership

Agents resolve multi-tier ownership structures, the kind that hide control across several layers and jurisdictions, into a clear beneficial-owner map. Our UBO mapping with AI guide covers the method.

KYB periodic refresh keeps business customers current

Instead of an annual scramble, an agent re-checks registry data, ownership, and risk signals on schedule, which is the perpetual KYC principle applied to businesses.

Why are agents deployed inside existing tools, not as a parallel system?

The instinct is to buy a shiny new agent console. The right move is the opposite. Agents are deployed inside Unit21, Jira, Salesforce, and the case-management systems your team already operates, for three reasons.

First, the audit trail has to live where examiners look. A decision made in a side tool and copied across is a decision you cannot fully defend. Second, your workflow, escalation paths, and QA sampling are already built around the system of record, and a parallel tool fragments them. Third, change management is survivable when analysts see agent dispositions in the queue they already use, rather than learning a new surface.

This is also where credentialing matters. An agent acting inside your tools needs an identity, scoped permissions, and instant revocation, the same model Zyphe applies to AI assistants: a dedicated service identity per agent with narrowly scoped access, so you can prove who did what and switch it off in one action.

How do model validation and AI governance rules apply?

Treat a compliance agent as a model, and the existing rulebook mostly already fits. In the United States, the Federal Reserve and OCC model risk management guidance, SR 11-7, expects you to validate a model, document its limitations, monitor it in production, and assign accountable ownership. The NIST AI Risk Management Framework adds the AI-specific governance layer: map the context, measure performance and bias, and manage the risks across the lifecycle. Treasury's own 2024 National Strategy for Combatting Terrorist and Other Illicit Financing acknowledges that AI, including large language models, has significant potential to strengthen AML and CFT compliance, while expecting it to be governed.

In practice that means version control on the model and prompts, decision-rationale logging on every disposition, ongoing monitoring of precision and recall, periodic validation against a human-reviewed sample, and human attestation on anything filed with a regulator. Data governance is part of this too. The NIST framework expects you to control the data an agent reasons over, which is far easier when identity data is not sitting in a single breachable store, as we cover in our work on decentralised PII storage. Manuel Tumiati, Zyphe's CTO and co-founder, frames the bar plainly in customer conversations: if you cannot reproduce the decision, you do not have a control, you have a guess.

Where does Zyphe fit, and what are the proof points?

Zyphe builds the identity and ownership foundation reasoning agents run on, and the agentic layer that acts on it. On the proof points, Zyphe reports L1 dispositions in around 12 seconds and four-tier UBO resolution in under 60 seconds, the two surfaces where manual review burns the most hours.

The architecture is the part competitors cannot copy cheaply. Identity data is sharded across more than 60,000 decentralised nodes using a 29-of-100 threshold scheme, the customer holds the encryption key, and Zyphe holds no master key, so the data an agent reasons over is not concentrated in a honeypot. Ownership resolution runs recursively down to low ownership thresholds, including opaque jurisdictions such as the BVI, Cayman, and the Marshall Islands handled through a specialist agent. Screening spans World-Check, ComplyAdvantage-equivalent feeds, OFAC, the EU consolidated list, UK OFSI, UN, and government-direct lists. That combination, decentralised data plus cited reasoning, is what lets the agent be both fast and defensible. If you are still choosing the underlying platform, the identity verification software comparison for 2026 and the AML compliance software guide are the place to start.

When should you not hand a review to an AI agent?

An honest pillar names the limits. Do not hand an agent the final sign-off on a filing. A suspicious activity report, a final EDD risk rating, or an offboarding decision should carry a human attestation, because accountability cannot be delegated to a model and regulators expect a named person to stand behind it.

Do not deploy an agent on a surface you have not instrumented. If you cannot log the decision rationale, version the model, and sample its output, you are not ready, and an unmonitored agent is a worse liability than a slow queue. And do not point an agent at genuinely novel typologies it has never seen without a human in the loop, because reasoning over an unfamiliar pattern is exactly where confidence and correctness diverge. The right frame is augmentation with attestation: agents dispose the clear majority and assemble the evidence, humans own judgement and the signature.

The bottom line

The fines that define this decade are not data-collection failures. They are review-capacity failures, and TD Bank's $3 billion is the headline example. AI compliance agents close that gap by doing the review work end to end, inside the tools you already run, with a cited audit trail that survives examination. They are not RPA, and they are not a black box: the ones worth deploying reason over real records and show their evidence.

Govern them as models, keep a human on the signature, and instrument the surface before you scale. Do that, and the agent becomes the reviewer your queue has been missing.

Book a 30-minute agent walk-through, or see how it works.

Related resources

- L1 alert triage with AI

- Can AI draft SAR narratives in 2026?

- UBO mapping with AI

- AML transaction monitoring in 2026

- AML compliance software in 2026

- Identity verification software comparison 2026

- Perpetual KYC: from photograph to video

Cited sources

- US Department of Justice, "TD Bank Pleads Guilty to BSA and Money Laundering Conspiracy Violations," October 2024: justice.gov

- FinCEN, enforcement and penalties: fincen.gov

- US Department of the Treasury, 2024 Request for Information on AI in Financial Services: treasury.gov

- Federal Reserve, SR 11-7 Guidance on Model Risk Management: federalreserve.gov

- NIST AI Risk Management Framework: nist.gov

Michelangelo Frigo (Co-Founder at Zyphe) Michelangelo Frigo is a privacy and identity infrastructure expert and co-founder of Zyphe.

Michelangelo Frigo (Co-Founder at Zyphe) Michelangelo Frigo is a privacy and identity infrastructure expert and co-founder of Zyphe.